Are you overpaying new joiners?

Our hiring market analysis shows a reduced pay gap in 2024; companies may be overpaying talent.

%2520(1).png)

Earlier in the year, our data showed us that it was the best time to hire in a decade, with the highest level of interest per role we’d seen since COVID. We’ve conducted further analysis, looking at what the bearing this has had on compensation dynamics in the market.

To find out more about hiring with Movemeon get in touch with our team here.

Using our proprietary data, we’ve analysed over one and a half million data points, and seen a seismic shift in the market. Two years ago, there was a large gap between the compensation candidates’ expected for a new job and how much employers were offering. Within just two years this has dropped to historic lows - suggesting that many companies “over-corrected” their salaries and are now effectively over-paying for new joiners.

In this article we look at how the compensation gap has changed over the last five years, driven primarily by supply-demand dynamics. We look at how this varies by company type, suggesting corporates have over-corrected their compensation, as well as Private Equity and Consultancies but for very different reasons.

Finally, we look at how this picture varies by alumni firm. McKinsey, BCG and Bain alumni have historically commanded a premium in the market, but we’re seeing early indications that this premium is decreasing. MBB expectations have only increased by a modest (and below inflation) level of 2% compared with 4% for the Big4 and 6% for boutiques.

Introducing the Movemeon compensation index and what it says about the market

Below you’ll see how the Movemeon compensation index has tracked over the last five years. We’ve analysed over one and a half million data points going back five years, looking at the gap between expectation and reality when it comes to comp. We see this as a measure of “friction” in the market, and an early indicator of inflationary pressures on wage growth.

For the numbers to make sense, it’s worth a quick recap of who’s in the Movemeon network;

- It’s global: our 75k members are based across the world, with our main hubs in UK, France, DACH, Middle East, APAC and US

- Everyone has worked in a leading consulting or accounting firm: 45% are ex-McKinsey, BCG and Bain; 30% are leading strategy firms; the remainder are the Big4

- They are future leaders and Board members: it’s well documented that McKinsey is the largest future leader factory in the world. The number of ex-consulting and accounting professionals leading companies (from Fortune 500 to PE and VC backed scale-ups) is astounding

How to interpret the numbers:

- 0-25: There’s only a small difference between candidate expectations and compensation offered In other words, it’s a highly efficient market

- 25-50: There’s a manageable difference between candidate expectations and compensation offered.

- 50-75: There’s a marked gap between candidate expectations and compensation offered - a high friction market.

- 75-100: There’s a large and unsustainable gap between candidate expectations and compensation offered - a very high friction market

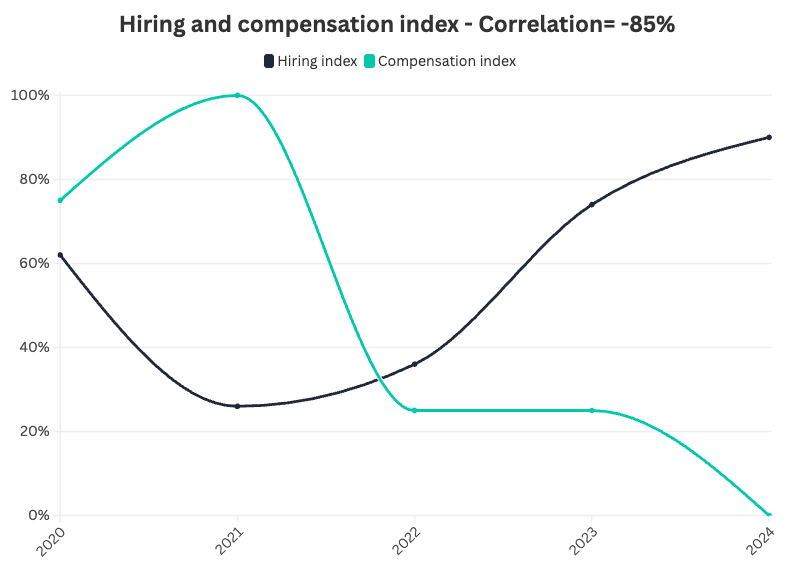

Supply-demand in the hiring market is the driver behind the compensation dynamics

When we plot our hiring and compensation indexes together, it’s clear there’s a very strong causal relationship (an 85% negative correlation). The more in demand ex-consultants are, the more their compensation expectations increase, resulting in a larger compensation gap between job offers and expectations.

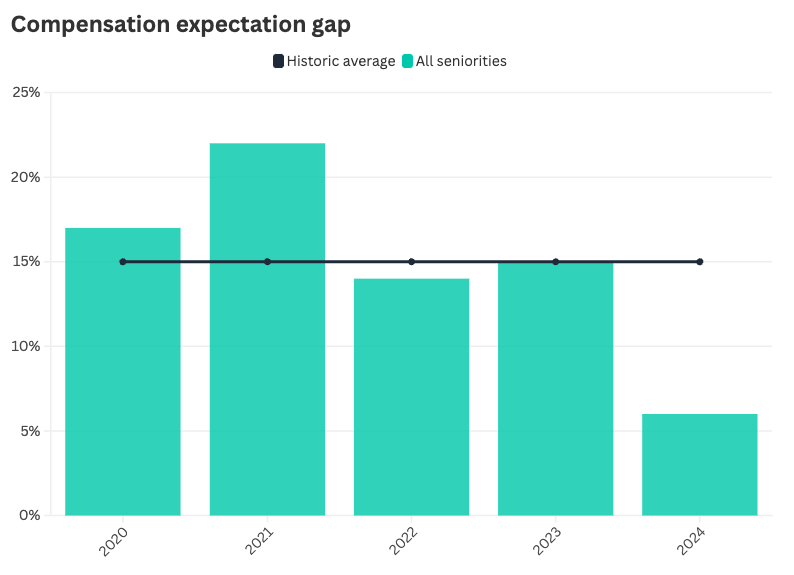

Are you now over-paying for new joiners? The compensation gap is at an all-time low

Over the past 5 years, we’ve seen the gap between expectations and job offers hit historic highs of 22% in 2021, before falling way down to 6%, -9% below the historic average.

We had assumed the drivers of the decrease in this gap were candidates re-adjusting their expectations downwards. This is historically what we’ve seen in very competitive hiring markets.

But this has not been the case. Over the past year, compensation expectations within our community have still increased at a healthy rate. The real driver of the expectation gap has been a very high increase in compensation being offered for jobs. This is clearly unsustainable in the longer-term, and feels like an over-correction in response to the higher consulting salaries and candidate expectations we saw in 2022-23.

For our latest salary information, you can view our benchmarking here.

Over-correction, hard to recruit talent, or paying for the best - how PEs, scale-ups, consultancies and advisories have reacted

When we look at our compensation index by company type, there are some very interesting trends.

Large corporates have a compensation gap of just 2%. This is much lower than historic averages, suggesting they have overcorrected compared with candidates’ expectations.

Scale-ups on the other hand have a gap of 13%. This is in line with historic averages and suggests that a focus on profitability combined with lower levels of VC-funding have ensured there hasn’t been an over-correction.

In the advisory space the picture is quite surprising. It’s been widely reported that it’s a tough market for consultancies, however, what our data shows is that those who are recruiting are prepared to pay a large premium - 8% in large consultancies, 5% in boutiques. We think this is being driven for two reasons: firstly, firms that are recruiting are growing, and as such are in a position to be paying for high performing (more expensive) talent; secondly, it is a hard market in which to attract ex-consultants given slow growth in the industry as a whole. To make it more appealing, bigger packages are being offered.

Finally, Private Equity is also paying a premium to outstrip expectations. This comes as no surprise and is also in line with historic norms in the sector. Private Equity is focused on attracting the very best, and as such is prepared to pay top decile compensations.

Compensation trends offer further evidence that McKinsey, BCG and Bain have been harder hit by the downturn than other strategy firms

When you look at how compensation expectations have changed by alumni firm, an interesting trend emerges. McKinsey, BCG, Bain alumni have seen the lowest increase in their expectations - a modest (and below inflation) figure of 2.3%. This is broadly in line with other strategy firms, but under half what we’re seeing alumni of boutiques and the Big4 demand.

Despite the higher increase in expectation from boutique and Big4 alumni, McKinsey, BCG and Bain alumni are still paid a premium of over 12% compared to the median compensation.

If you’d like to find out more about how Movemeon can support your hiring, please get in touch.

Where talent meets opportunity

Our latest articles

The Hiring Index closed Q2 2026 at 39, its tightest reading since October 2023, after a soft April and May, as new freelance demand and rising job supply drove a sharp June tightening. Freelance and permanent demand are now converging, Private Equity remains the strongest company type on every measure, Corporates and Advisory are building real momentum of their own, and Scale-ups remain the one company type still finding its footing.

Meta UK's chief exec (ex-McKinsey, ex-Sequoia) shares a career framework built on rising complexity and expanding influence rather than titles, plus advice to stay close enough to real work to catch mistakes, including bad AI outputs. She ties this to Meta's strategy: WhatsApp agents aim to restore personal trust at scale, AI is expanding jobs rather than cutting them, and targeted fixes beat blanket bans.

%20(1).jpg)

The Chief of Staff role has become a key early hire in PE-backed portfolio companies, helping CEOs create leverage in the critical post-acquisition phase. It plays a central role in driving Value Creation Plan execution, strengthening investor communications, and improving leadership team effectiveness. This article explores why demand for the role has increased and what good looks like in practice.

Join our ecosystem to discover unique opportunities and advice

100,000+