Everything you need, at a glance

Our Insights are detailed and well researched. They keep a pulse on what’s happening in the market and allows you to stay ahead of the curve.

Sign up to our newsletter to get exclusive insights and never miss an article.

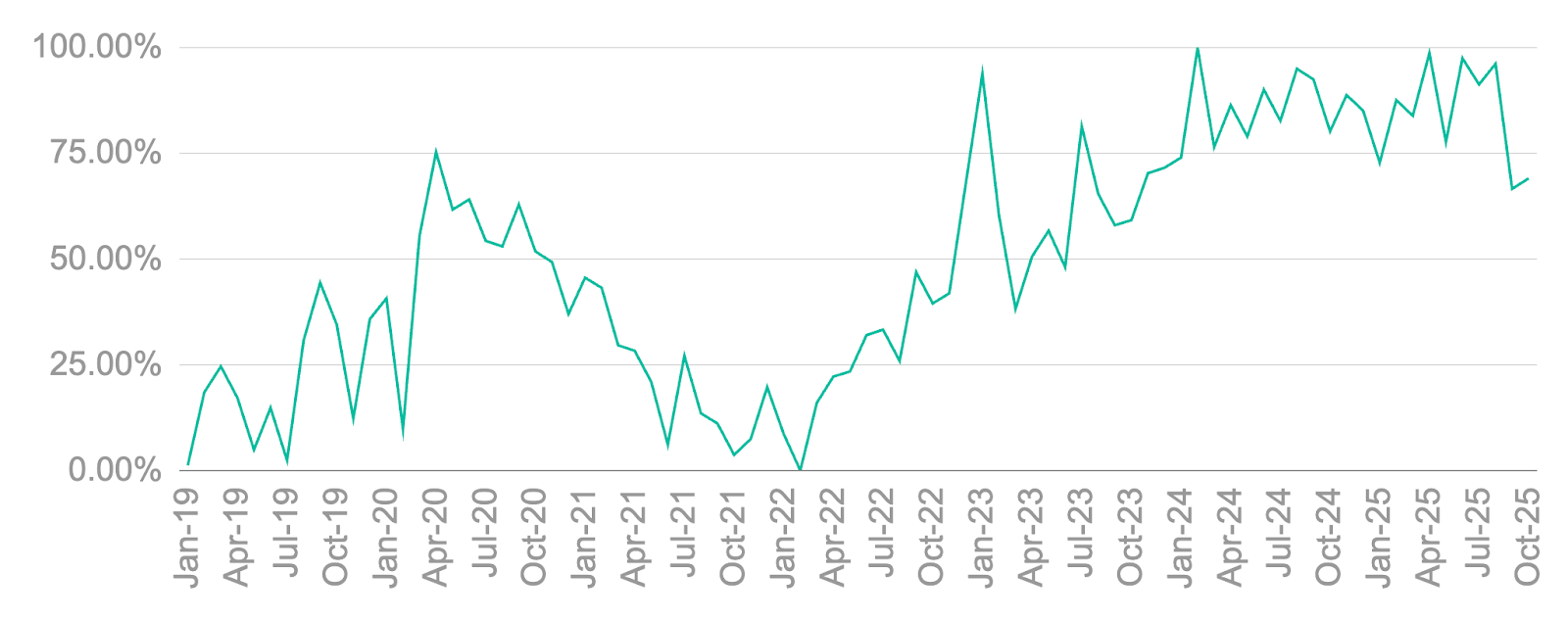

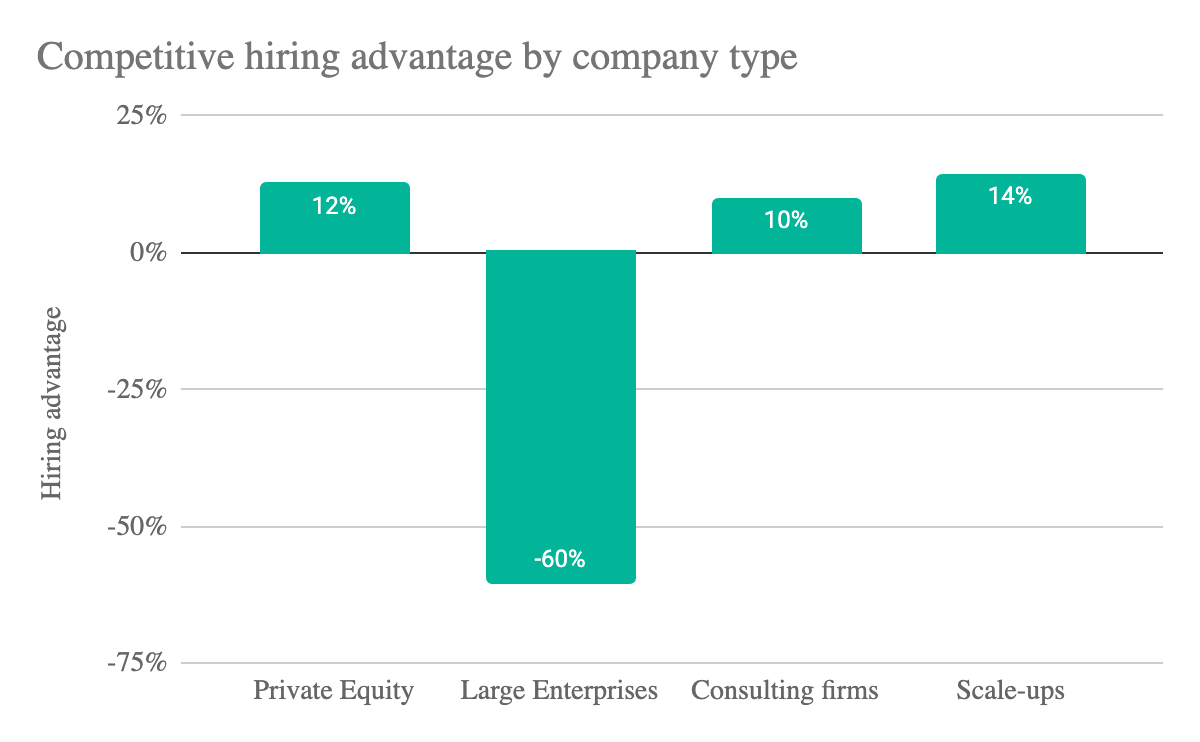

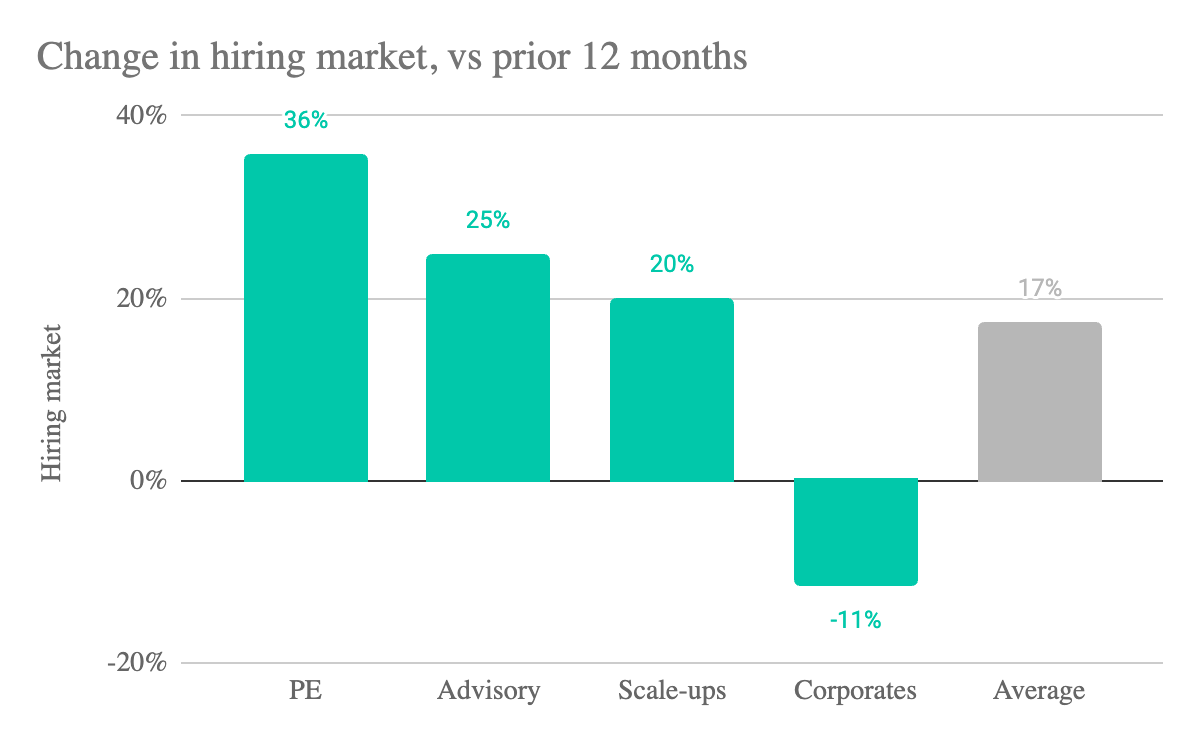

A record quarter for Private Equity deals sees a sharp hardening in the hiring market

Talent supply tightens as PE demand surges: Inside Q4’s hardest hiring market in two years, where Private Equity accelerates, scale-ups hold steady, and Large Enterprises struggle to attract strategy and transformation talent.

This report marks the fourth installment of Movemeon’s Quarterly Hiring Analysis, a regular update designed to help hiring managers and candidates stay ahead of the market across Private Equity, VC-backed scale-ups and large Enterprise businesses. Our insights are powered by over 2.2 million data points from the Movemeon platform, giving you a clear picture of how candidate interest and hiring demand are shifting.

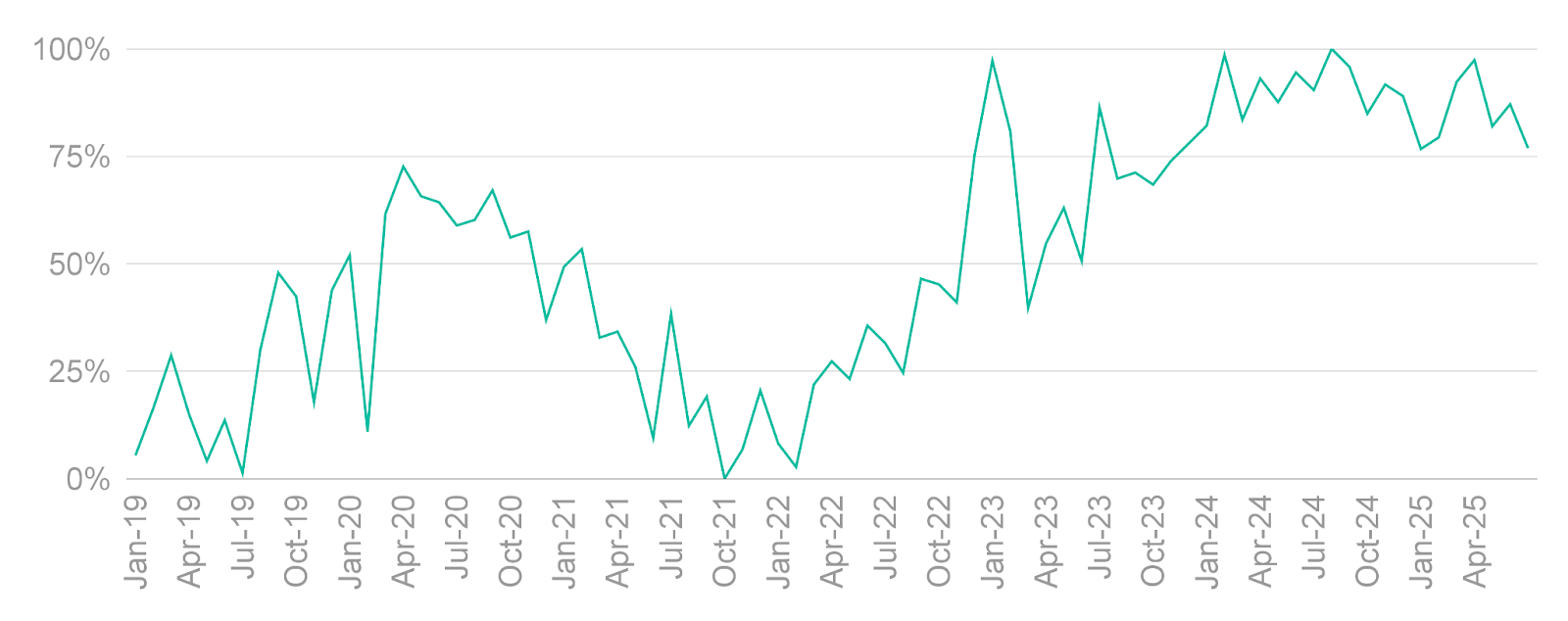

At the heart of this analysis is the Movemeon Hiring Index, a scale from 0 to 100 that reflects how attractive the job market is for employers. In short: a higher index means higher candidate interest per role. When the economy slows, candidate supply tends to rise, pushing the index up. When hiring demand picks up and candidate availability falls, the index drops.

The Strategy and Transformation Hiring Index dropped to 68% this quarter. This is the lowest value, signalling the hardest market to hire in, that we’ve seen for two years.

The driver of this hardening of the market seems to be two fold. Firstly, there has been a sharp uptick in demand for talent from Private Equity. The combination of an increase in deals (Q3 was a record), and the increasing focus on using talent as a key driver of Portfolio business performance, has resulted in the increase in demand. Secondly, we’ve seen candidates less attracted to working in Large Enterprise businesses, resulting in a harder market for Corporates to hire.

We conclude the article by reflecting on what we think might happen next. In short, given the amount of PE Funds awaiting to be deployed, we find it highly unlikely things will abate. If anything we expect this market to continue to harden into Q1.

The Movemeon talent index

The Index is designed to give employers a read on the talent market: is it competitive? Are candidates open to new roles? Are certain industries or job types seeing more traction than others?

Below is how the index has changed over the last five years. For context, it's worth understanding who the Movemeon community are:

- It’s global: our 90k members are based across the world, with our main hubs in the UK, France, DACH, the Middle East, APAC and the US

- Everyone has worked in a leading consulting or accounting firm: 45% are ex-McKinsey, BCG and Bain; 30% are leading strategy firms; the remainder are the Big4

- They are future leaders and Board members: consultancies make up six of the top eight "CEO factories" (companies whose alumni become CEOs of the largest businesses). And this isn't constrained to just large businesses, with a disproportionate number of unicorns founded by consulting alumni

In terms of interpreting the numbers:

- 0-25: a very hard market to hire in. Focus on retention, as replacing people is going to be hard.

- 25-50: a hard market to hire in. Be proactive and start talent pipelining for key positions.

- 50-75: a good market to hire in. Start looking to take advantage of the market, and strengthen key positions.

- 75-100: an exceptional market to hire in. Look to bring in exceptional talent that you’ll only get a few chances to snap up.

Demand now outstrips supply as the market tightens

The hiring index has fallen to 68%, the lowest level since October 2023, signalling the most challenging hiring environment in nearly two years.

For the past 12 months, the index had held stubbornly above 75%. In our last quarterly analysis, we noted that this resilience persisted even as hiring activity increased, suggesting there was still an oversupply of candidates in the market.

So what has shifted in Q4 2025?

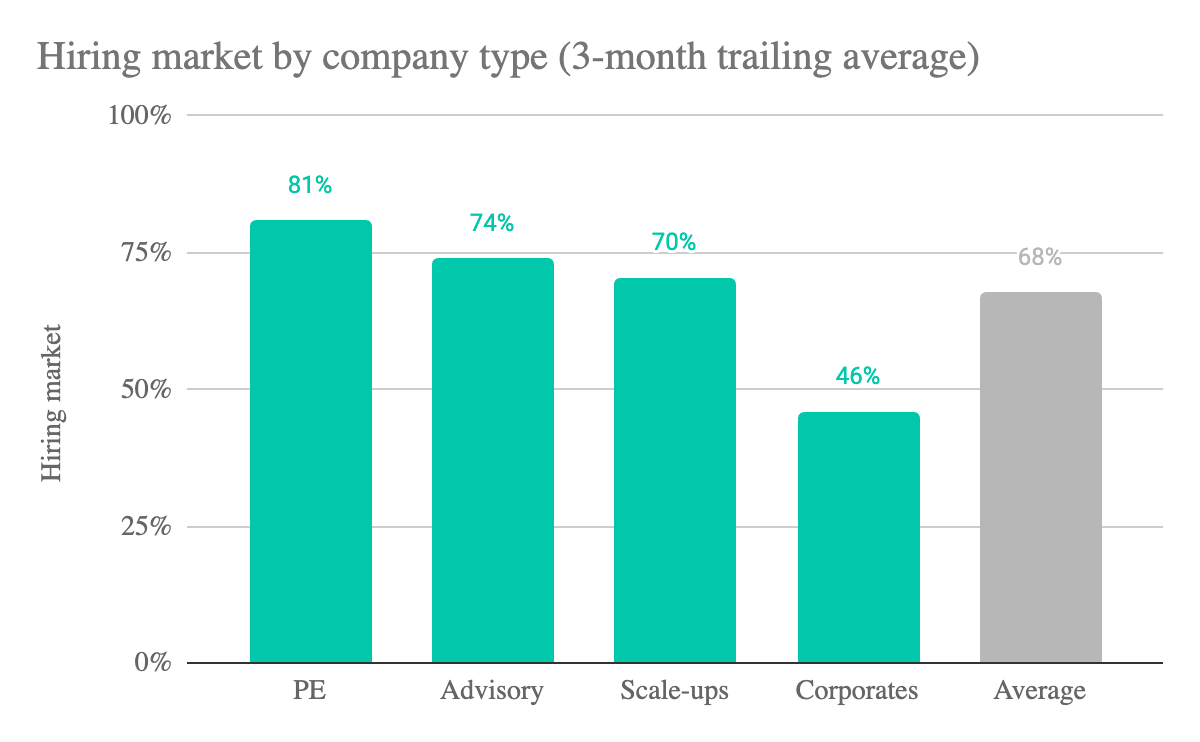

To unpack this change, we analysed the hiring index by company type to understand the underlying dynamics driving the tightening.

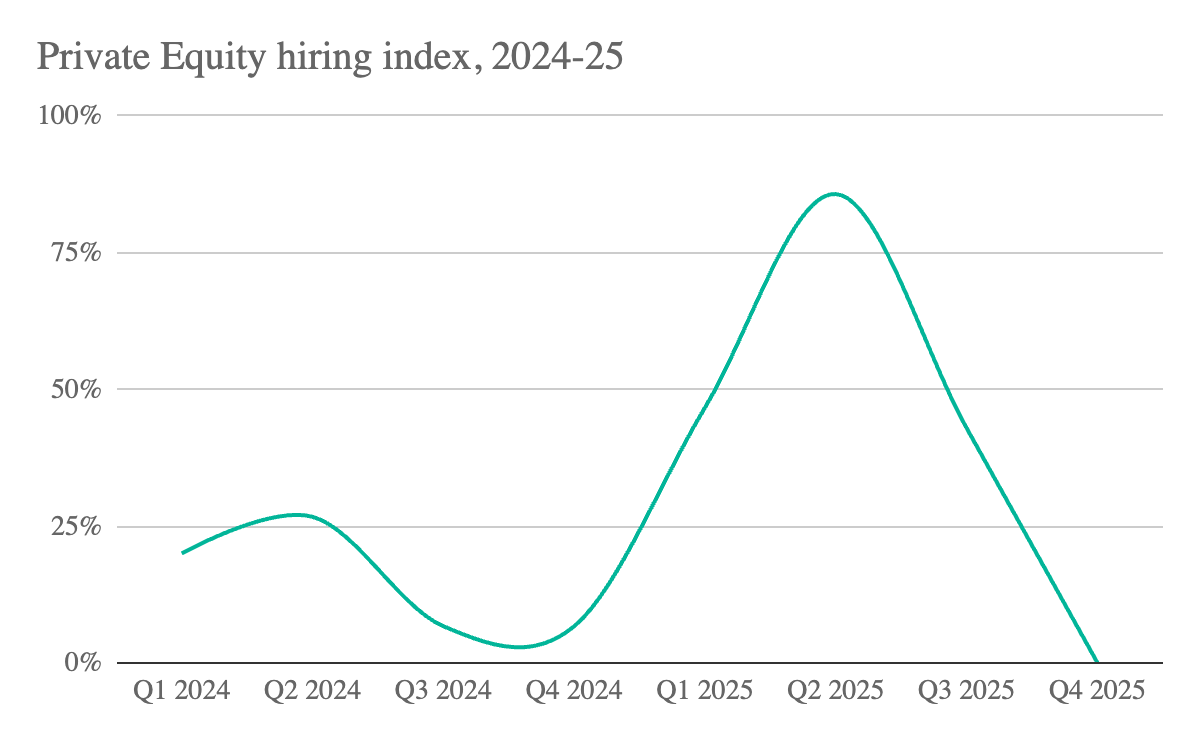

Private Equity is driving a surge in hiring demand

A hiring index of 68% is the lowest we’ve seen since October 2023, signalling the hardest market to hire in for 2 years.

Whilst we’ve seen some variability in the PE hiring index, the difference over two quarters has been profound. Moving from 80% (a good market to hire in) to 4% (a very hard market to hire in) in just 6 months, shows how quickly the market can shift.

What’s driven the rapid turnaround in PE. We believe it’s two-fold:

- Q3 was a record of capital deployed in PE

- Continued focus on talent to drive operational improvement across the deal lifecycle

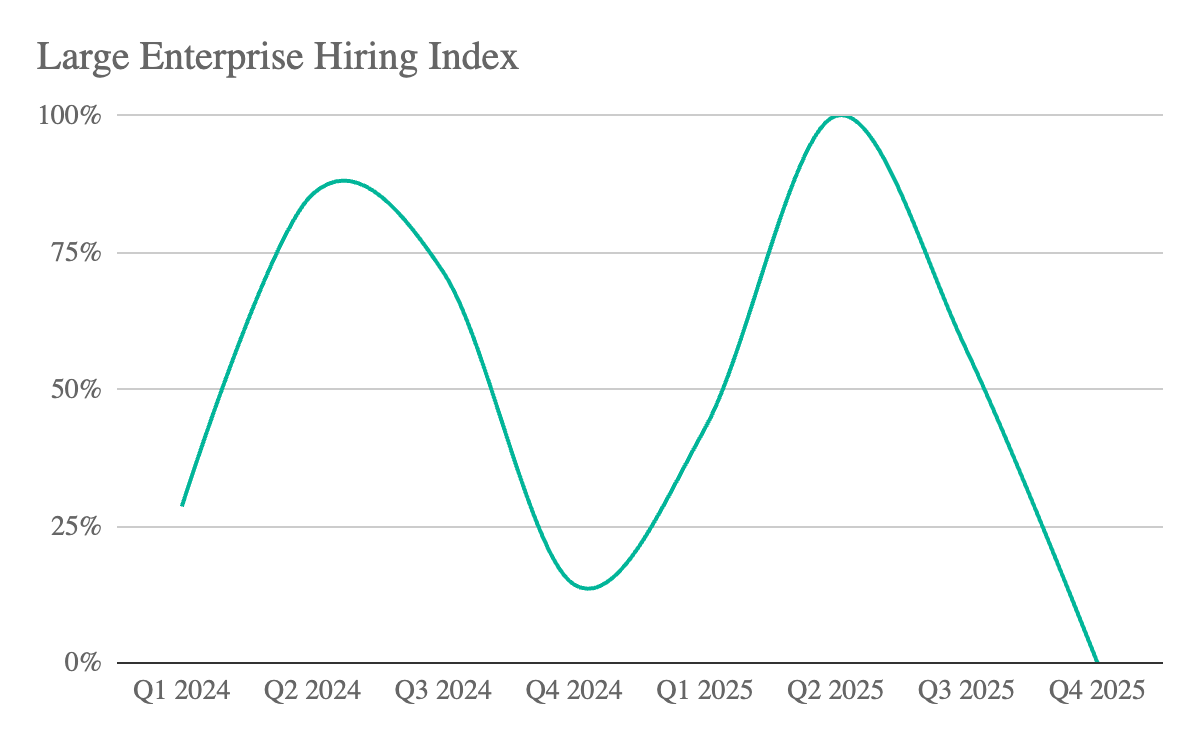

Large Enterprises/ Corporates

We’ve also seen the market tighten for strategy and transformation talent within Large Enterprises and Corporates.

For Enterprise businesses, the sharp reduction in the hiring index appears to be driven less by increased hiring demand and more by a decline in candidate interest.

Our analysis of the hiring index by company type, a useful proxy for how attractive different organisations are to candidates, shows a clear pattern. While scale-ups, PE firms and consulting businesses perform similarly, Large Enterprises face a significant disadvantage when it comes to attracting strategy and transformation talent.

What’s next

Given the amount of Private Equity funds ready to be deployed, we find it very unlikely that things are going to slow down for the foreseeable future. If anything, given the number of Funds we’ve been speaking to who have mentioned deals on cusp of closing, things are likely to accelerate into Q1 next year.

To find out more about hiring with Movemeon get in touch with our team here.

.jpg)

Bringing a refreshing approach to hiring in the US: An interview with Movemeon’s General Manager

Movemeon’s US GM on his career journey and how the firm is redefining hiring in the consulting and PE market.

Can you tell us a bit about your own career journey and what led you to take on the role of General Manager for Movemeon in the US?

I began my career working in the experiential marketing world, delivering experiences for some of the worlds largest brands and sports properties. We aimed to deliver best in class experiences for fans, consumers, and clients. I was very fortunate to work with many leading marketeers, whose attention to detail and client handling skills have been a strong foundation throughout my career. Since then, I have been leading and scaling disruptive teams and businesses, predominantly at the intersection of HR and technology, often working alongside first class ex-consulting minds.

Prior to Movemeon, I relocated to the US to launch and scale a high performance team at a fast growing UK tech company. I knew of Movemeon as they sourced some incredible candidates and placed some pivotal roles for the firm. When I heard they were hiring a GM, and looking to expand into the US, it felt like the perfect opportunity to draw upon so much of my experience and skillset as well as provide some cultural translation.

What was the vision behind bringing Movemeon (with its specialist hiring, consulting & interim services) to the US market?

I’m very lucky - Movemeon has an incredible track record, candidate network, list of clients and brand recognition in Europe. The team had already spent a few years laying the groundwork in the US by building out our candidates and getting global referrals to clients. Given the success of the business in Europe, expanding into the largest and most mature consulting market was a matter of ‘when’ not ‘if’.

In your experience, what does Movemeon do differently or better than traditional hiring / consulting firms in the US?

What sets Movemeon apart is our engaged network of over 100,000 candidates globally in a very specialist area - current and former strategy consultants. On top of that, our tech driven delivery model means we can engage with better candidates faster than traditional methods.

Can you share some case studies or stories from US companies that illustrate how Movemeon solved a tough hiring or consulting problem?

On a recent call with the Head of Talent for a well known large cap PE firm, they mentioned they were currently hiring for a very specific role on the operating team and gave a one line description of a candidate they were looking for. Within 72 hours we had surfaced the perfect candidate whose background and resume literally “wrote the job description”.

In another recent scenario, a client rang us to say they’d been struggling with a very important role for almost a year, whilst it was slightly outside of our wheelhouse, we were able to agree a model that worked for both sides, and through our network, pull together a very strong shortlist within two weeks. We currently have a candidate in the final round for the role.

If you had to sum up in one sentence what companies in the US should expect if they work with Movemeon, what would that be?

A refreshing approach to a traditionally antiquated industry, through a high-touch and personal service, driven by a tech delivery model.

Looking ahead, what are your ambitions for Movemeon in the US over the next few years - whether that’s new services, industries, or ways of working with clients?

The US is Movemeon’s fastest growing market globally, both on the candidate and client side, and it’s only going to continue accelerating. We’re particularly seeing huge growth in the Private Equity vertical and we’re already growing the team to support, watch this space!

Looking for the best talent in the US? Let us help.

.png)

The new age of consulting - how client demands are changing

Consulting disrupted: Clients demand flexibility, execution expertise, and lower fees as traditional firms face competition from interim executives and agile consulting teams.

Consulting is going through a seismic shift. After years of double-digit growth, the combination of a tough macro-economic climate and more alternatives in the form of independent consultants and in-house ex-consulting talent is challenging the very foundations consulting is built on.

In this article, we talk through how we’re seeing client demands for consulting and advisory support shifting, and what this means in terms of a new landscape of advisory support.

If you’d like to know any more about how you’d deploy either model, or would like to see some example projects get in touch with our team here.

Is consulting no longer recession-proof?

The old adage explains that you need consultants in the good times and the bad. As such the industry had historically been seen as largely recession-proof. This "professional services” resilience has resulted in an interest from private capital markets over the last few years, but is this being challenged in the consulting market?

Ten years ago, HBR first referenced “consulting on the cusp of disruption”. The post-COVID boom resulted in pay rises, over-hiring and an increasing reliance on non-core strategy work. This meant few in the industry were prepared for the correction in 2022-23.

We highlighted what we saw in the industry, both from a client perspective and in the consulting firms:

On the client side:

- There’s increased need for deep industry experience

- Fees have reached unsustainable levels and typical delivery models are too rigid

- Quality isn’t what it used to be

Which has started to have knock-on effects to the consulting industry:

- Top performing partners leaving to launch boutiques

- Rise of quality in the freelancer market

- Change from AI on the horizon

How is the market now responding?

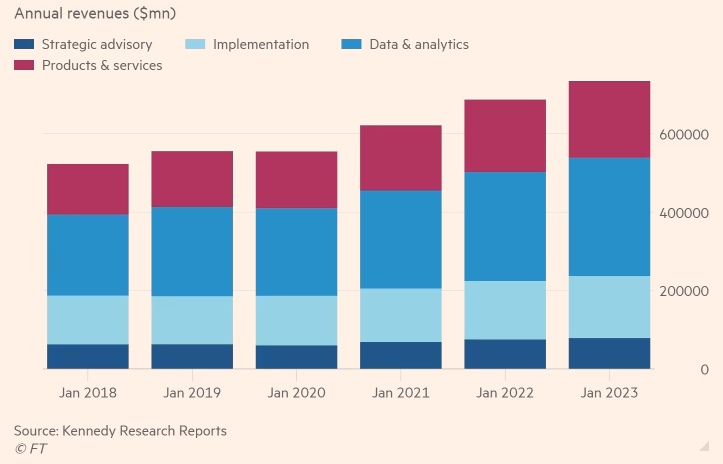

The growth of consulting firms in the post-COVID era was driven by providing more advice outside of the core of strategy. Clients had found returns on bringing in expertise to help drive implementation, analytics and new products/ services. By January 2023, the Kennedy Research Reports found that strategic advisory had fallen to just 10% of the consulting industry’s revenue - from 17% just five years earlier.

The 10% of strategy work, which grew very little over the last five years, is seeing less disruption: Large Cap PE funds are still turning to McKinsey, BCG and Bain for due diligence, and development of the Value Creation Plan; the Boards of large corporates and enterprises are still choosing to get the assurance of one of these firms on the once in a decade decisions.

However, for longer-term implementation, transformation projects and new market entry projects, we’re seeing a shift away from the traditional firms. PE and Enterprise clients are conscious they don’t have the capability or capacity to deliver these in-house. They are also aware that experts who have overseen similar projects countless times will help them avoid the pitfalls and maximise ROI. However, they are unwilling to spend the fees commanded by the traditional firms - especially when the delivery models designed around strategy projects (Partner only part-time; EM+2 team) are so rarely flexible, and the Partners at these firms often don’t have real operating experience.

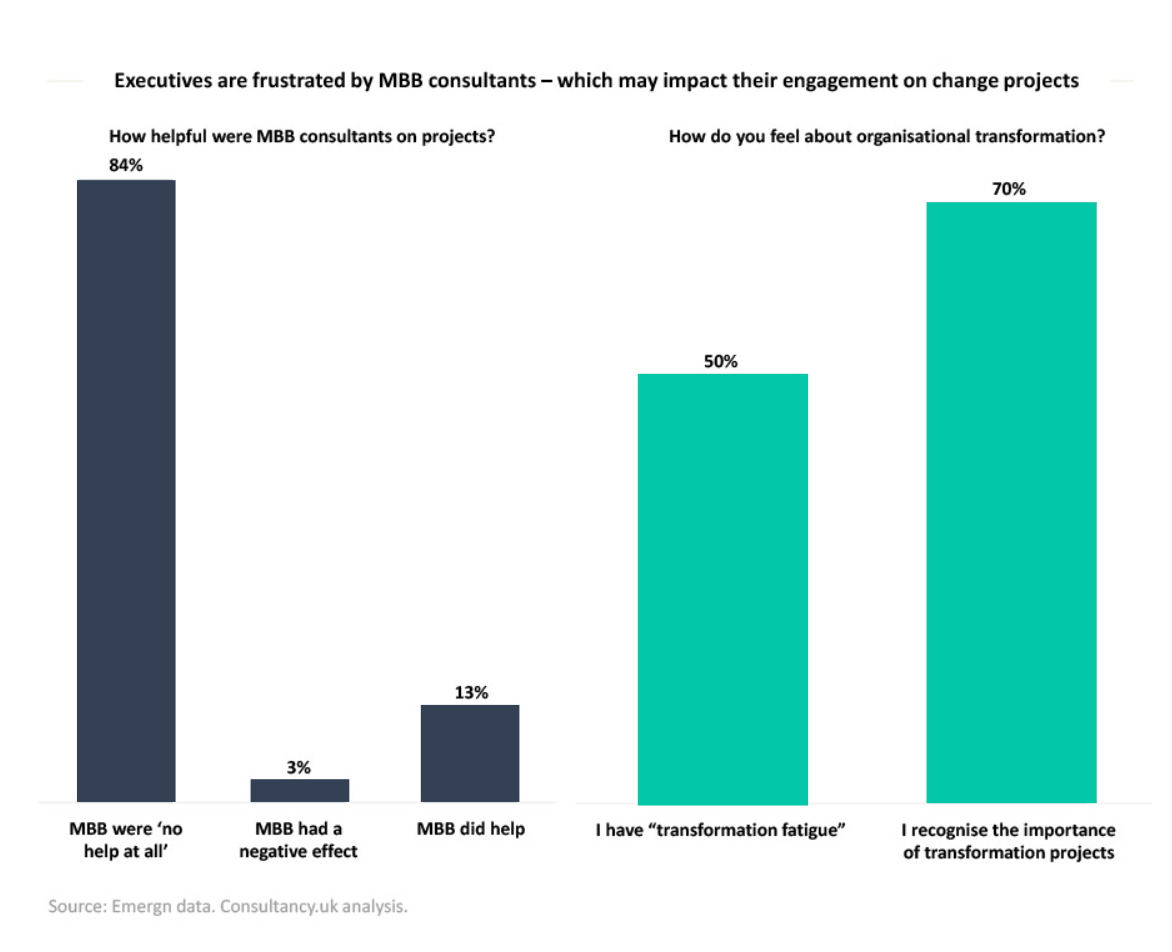

This has meant that very few believe MBB defend their cost when implementing large change programs - 84% of executives saying that MBB were “no help at all” in a recent Emergn survey about change projects:

A new breed of competition and the risk of marketing myopia

Theodore Levit is often quoted by consultants. They’ve explained to many clients that focusing on delivering value must always usurp the pressures of continuing to sell current products and services. Kodak and Blockbuster are often cited as examples of not doing so.

It’s definitely time the consultants heed their own advice. Consulting for many years has been able to defend its price point through exceptional solutions and effective communication of these. There’s almost a bit of magic about how they get there. However, it is fundamentally a people business. And we’re increasingly seeing clients shifting towards other ways to access these people.

Twenty years ago the consulting alumni world was still pretty small. The firms were growing but not many had been through their intense training and coaching. As they’ve continued to grow, the alumni networks and number of “consulting trained” experts has grown exponentially. We’ve seen rapid growth for two types of advice: interim experts and agile consulting teams.

Interim experts - embedded senior executives with deep operating experience

Typical roles and cost: The majority of the demand we find for interim executives are either roles responsible for overseeing a change (Chief Transformation Officers / Head of PMO) or are bringing in deep expertise (Chief Procurement Officer, Head of Pricing / Sales Excellence). The transformation roles tend to be 6-18 months in length; the experts normally 3-5 months.

Typical profiles: A combination of ex-top tier consulting (ensures they can effectively work alongside the executive team) and deep operating experience. They’ve typically worked in industry in a senior or executive role for 5-10 years. This means they know what it takes to deliver real change. Day rates will vary a lot on profile and length of project, but are typically £1.5k - £4k.

What they offer that a consulting firm can’t: There are two main drivers: time and “operating experience”. For time, interim executives are the equivalent of a “Partner” on a consulting project. Typically with Partners, they are spread between multiple projects and as such you likely only get 1-2 days of their time a week. With an interim executive, you get them 100% of the time. Secondly, they all bring deep “operating” experience. Many consulting Partners have worked their way up through consulting, without having held senior roles in PE or Industry.

Agile consulting teams: flexible, specialist, end-to-end

As part of our own consulting offering, we’re seeing client demand and ex-MBB Senior Partner supply converge across a number of specialism areas as outlined below.

Typical projects and cost: Complex decisions that need deep expertise. They are typically the main 2-3 initiatives post strategy development, and include new market entry, operational improvement, organisational design, procurement review, pricing strategy etc. They are high-impact projects that often have a big bottom-line impact. Cost varies on team composition, but typically ranges between £20-50k per week.

Typical profiles: Agile consulting firms are often led by an ex- senior Partner from McKinsey, BCG, Bain or equivalent, who leverages deep functional expertise from interims (as above).

What they offer that a consulting firm can’t: While the ex-MBB Partners ensure the same level of assurance that you’d see with one of the large consulting firms, they are able to offer much more flexible models and deeper industry / operating experience. The flexibility starts with themselves, with potential to be anywhere between 100% staffed on a project to hardly involved - and they will flex up and down the team over the project lifetime. They also offer deep industry expertise, and are able to assemble an exceptional team of interims with backgrounds spanning a plethora of consulting firms and with the requisite functional / industry operating experience.

If you’d like to know any more about how you’d deploy either model, or would like to see some example projects get in touch with our team here.

Agile consulting delivering value in practice

To expand on this with some concrete examples from our own work, we’ve summarised some key challenges we’ve recently seen from clients and outlined why the agile consulting approach worked below:

Operational improvement for a PE-backed manufacturing business

A nationwide UK manufacturer, owned by a £50bn AUM PE fund, needed rapid EBITDA uplift across its product portfolio. An agile consulting team was assembled by Movemeon Consulting to deliver impact within 2 months, with a team comprising:

- Partner: Ex-McKinsey Senior Partner with over 20 years’ experience in operational improvement and manufacturing diagnostics;

- Engagement Manager: 5 years at McKinsey, followed by senior strategy and PE-backed operational roles;

- Associate: Ex-Bain Manager with deep regulated manufacturing experience;

- Analysts: Ex-LEK and Bain, both with operating experience and strong financial modelling / PE exposure.

The challenge: Performance varied widely across sites, with underperformance dragging on overall profitability. The client needed a clear diagnostic and pragmatic turnaround roadmap, executed at speed.

The outcome: The team’s diagnostic identified 7 underperforming sites, developed tailored turnaround plans, and began embedding operational workstreams. The impact was so strong that the client permanently hired the EM from the agile team to continue the transformation.

Why agile consulting worked: This bespoke mix of ex-MBB consultants and operators, led by a senior industry expert, gave the client tier-one insight at pace and cost-efficiency, without the overhead of a traditional consulting firm.

The result: Sustainable operational improvement, delivered by a right-sized, high-calibre team.

Commercial strategy and PMI for a global consumer business

A $5bn consumer business, carved out by a $100bn+ AUM PE fund, required a new commercial strategy and seamless post-merger integration to set up the business for growth. A lean, agile consulting team was assembled to deliver across 12 months, consisting of:

- Sales Excellence & Transformation Director: 20 years’ operating experience at Expedia and Whitbread, with deep expertise in sales excellence, transformation, and commercial operations.

- Senior Consultant: Former BCG Senior Consultant with 5 years’ operating experience in high-growth tech businesses, notably having led PMI for consumer-focused businesses in 20+ countries.

The challenge: The carve-out created a need to stand up commercial functions from scratch, while simultaneously implementing a robust sales excellence strategy to accelerate performance across global markets.

The outcome: The agile team successfully established commercial functions, delivered a scalable sales excellence strategy, and ensured seamless integration across units. The impact was lasting - the client made a permanent hire of the Sales Excellence & Transformation Director to continue driving results post-project.

Why agile consulting worked: By combining a former BCG strategist with a seasoned transformation operator, the client gained a tailored, high-impact team able to deliver both strategic clarity and operational execution - faster and more effectively than a traditional consultancy.

The bottom line

Transformation isn’t just about ideas - it’s about embedding change. Strategy may set the direction, but execution decides whether the journey is completed.

Consulting firms are built around making the key and critical strategic decisions. And they are extremely effective at doing so. However, when it comes to driving the change and transformation, the operational expertise and flexibility offered by interim talent and agile consulting teams is increasingly out-competing the consultancies.

If you’d like to know any more about how you’d deploy either model, or would like to see some example projects get in touch with our team here.

An AI-driven boom for advisory firms? What’s going on

Advisory hiring is surging despite AI’s disruption: large firms and boutiques see rising demand, while clients seek guidance on integrating AI and redefining workforces.

The death of consulting? Not according to the hiring data

It’s clear that AI poses existential threats to the current consulting operating model. At the core of the consulting proposition is synthesising complex data, market intelligence and driving to clear recommendations. All things that AI will be able to do better than humans. It’s not an if; it’s a when.

Our quarterly market index highlights how hiring trends are evolving, with a particular focus on the near-term outlook for advisory roles.”

In our September analysis, we were very surprised to see that Advisory businesses hiring demand is outstripping that we’re seeing in Large Enterprises. Interestingly, it is also outstripping the demand we’re seeing in scale-ups (a market you’d expect to be seeing a boom from AI).

So what’s going on?

The risks posed to consulting by AI are widely discussed, and for good reason: At the heart of the consulting proposition lies the ability to synthesise complex data, interpret market intelligence and drive towards clear, actionable recommendations, precisely the areas where AI is advancing fastest. It’s not a question of if AI can outperform humans in these tasks, but when.

This advancement raises existential questions about the industry’s current operating model, particularly for leaders thinking about project staffing, protecting margins, and developing the next generation of partners. The immediate concern for many is how this is impacting talent in, or looking to join consulting firms- why hire more people if AI can do the same things more cheaply?

But this isn’t what we’re seeing. In fact, hiring demand is up within consulting.

Despite the noise around disruption, our data shows a very different short-term story. Hiring demand across the advisory sector has been rising sharply compared to last year. Initially, we hypothesised that this growth was concentrated in boutique firms, smaller, more agile players pivoting to build AI-focused propositions. If true, this would suggest not a real increase in overall demand, but rather a talent migration away from large consulting firms into specialist boutiques.

However, the numbers told a different story. Hiring demand has risen by 21 percentage points in large firms, and by a more modest but still significant 9 percentage points in boutiques. In other words, demand is not confined to specialists, it’s happening across the board.

Why? Clients are grappling with the same questions about the impact of AI

This trend points to a critical dynamic: The immediate impact of AI on consulting has been overstated. For many firms, the boom is being fuelled by client demand for guidance on exactly the issues senior leaders are worrying about themselves:

• How to integrate AI into core operations.

• What it means for workforce design and resourcing.

• Where value creation opportunities lie in an AI-enabled world.

Implications for consulting leaders

This raises three important considerations for leaders in the consulting industry:

1. Delivery models are shifting, but they’re not collapsing

While AI will automate traditional “analyst tasks,” the near-term demand is for advisory capacity, client guidance, and operating model design. This creates space for firms to rethink the shape and scale of delivery teams, rather than fearing their wholesale replacement.

2. Margins are still defensible, but only when value add is clear

Clients are willing to invest in external expertise, but expectations are shifting. Firms must be ready to demonstrate the distinctive value of human insight alongside AI-driven efficiency, ensuring pricing models reflect both. We see this playing out in the mandates we see from consulting clients, most of whom are looking for deep expertise in a specific functional or industry area, not general capacity augmentation.

3. Talent development cannot be an afterthought

If the AI evolution continues as expected, the real long-term risk is not staffing cuts, it’s a potential skills gap. If AI erodes the traditional training ground of junior consultants, firms will need to ensure the next generation develops judgement, nuanced thinking, client relationship development skills and leadership capability.

Is this a temporary uptick, or a longer term hiring trend?

The jury’s still out on whether this demand surge is a short-lived reaction to AI uncertainty or the beginning of a new growth curve for consulting. But one thing is clear, in the short term, the consulting sector is experiencing a boom, not a bust.

Consulting leaders should resist the temptation to over-correct. Instead, they should focus on building hybrid models, protecting margins through clear value articulation, and reimagining training for future leaders.

What’s certain is that AI will reshape consulting, but for now it’s fuelling demand, not reducing it.

Redefining networking: How to build lasting career momentum

In this article, ou co-founder Rich breaks down 8 simple, practical tips to reconnect with your network, build trust, and stay front of mind for opportunities, all while giving as much as you gain.

Most of us dread “networking”, the awkward small talk, the forced introductions, the feeling of wanting to disappear under the canapé table. But Movemeon’s co-founder, Rich, argues that this isn’t networking at all. Find his advice below!

Picture the scene.

You've just arrived at a corporate venue. You've picked up your name badge. You're thrust into a room full of people you don't know.

You feel obliged to try & scurry around introducing yourself to folks you'll probably never see again. If you're honest with yourself, you're tempted to hide under the canapé table. And you'll definitely find an excuse for an early exit.

This is what most people picture when we use the term "networking". And it understandably makes most of us want to run a mile.

What's more, it's almost totally ineffective. These aren't people who know you. So how can they trust you or advocate for you?

So what is a better definition?

"Keeping in touch with people who know your capabilities & will advocate for you."

Typically these are people you've worked or partnered with in the past. Probably peers or former bosses. People who know you & like you. Or they might be people that those people have introduced you to with their backing.

When you reframe networking like this, your shoulders relax. In fact, you can picture that re-connecting with these people might actually be quite enjoyable.

It's the network of their network where most opportunity lies.

Don't get me wrong. If you keep up with this group, it's not uncommon that one of them will give you a call at some point and ask you to join their team. (The timing might not be right. The opportunity might not be right. But it's always great to be asked).

Much more likely is that they'll think of you when someone in their network is chatting to them. It could be that their friend wants an expert point of view. Or a supplier recommendation. Or that they're building a new team and asking for suggestions. Either way, you'll be front of mind for an introduction.

So what are my 8 tips for re-booting your networking and making it both sustainable & impactful?

- Write a short list. 15-30 people who know your capabilities (ideally peers or seniors).

- Put them in a spreadsheet / Trello board / other type of simple tracker.

- Don't be scared to get back in touch with people you've lost touch with - you'll be surprised just how many are happy to hear from you.

- Make a simple, realistic goal. E.g, meet 1 person per month (assuming you're in a full time job; stretch this target if you're actively job seeking).

- Don't be transactional. This is about building trusted relationships.

- Do be intentional. People who know & trust you are happy advise or support you.

- Be resilient & systematic. If they didn't reply to your first message, follow up 1 week later (it's not because they dislike you; it's because they're busy & forgot to email back).

- Give as well as take. Make thoughtful connections for these people. And lean into people trying to network with you. Remember how you feel about that person who is only in touch with you when they want something (we all know one). Don't be that person. Instead, "pay it forward" - good karma quickly comes around.

Implement these 8 simple tactics to make networking easy, enjoyable & accelerate your career.

About Rich and how you can work together

Rich started his career at McKinsey before working as a freelance consultant alongside co-founding Movemeon. Over 15 years he's helped over 5,000 organisations to hire - organisations of all sizes in all industries, globally - and developed a unique overview of what works to build successful, happy careers right up to CEO level.

He has always given advice via LinkedIn message to anyone who's asked for it. And in 2025 - encouraged by his network - he formalised this through the creation of OnUpBeyond .

The 2025 pilot of his career advisory sessions was massively oversubscribed, despite a price point in the thousands 000's. Those who managed to grab a place consistently reviewed the experience as 5*.

In July 2025, he relaunched his support in a truly accessible way via The Career Momentum Hour.

- Ask your questions for expert advice tailored to you.

- Weekly advisory sessions - listen in live or catchup in your own time via recordings.

- Regular senior guest speakers from CEOs, to Investment Directors to startup Founders to Exec Search bosses.

- Peer mentorship - your champion & trusted sounding board.

.jpg)

The job market heats up: Hiring demand hits an 18-month peak

Hiring demand surges, talent supply shrinks: Inside Q2’s shifting job market where Private Equity booms, advisory hiring accelerates, scale-ups rebound, and corporates face mounting pressure to compete

Q2 market index reveals shifting dynamics in talent demand

Hiring demand for permanent roles is at its highest we’ve seen for 18 months. We saw an initial strengthening in the market last quarter, but expected this to have dropped given the macroeconomic environment and the impact of tariffs.

However, after a small initial dip in May, the hiring market has continued to grow, reaching its 18-month peak in Q2 2025. As the hiring market has strengthened, the talent index (measuring the supply of great talent on the market) has started to drop. Between Q1 2024 and Q2 2025, the market index averaged at an all time high of 90, before dropping to 75 in July 2025. This is only slightly above the average for 2023 (70), when companies were still struggling to hire post COVID and the Great Resignation.

In this article we look at how different types of companies are being affected by these broader trends. We find that Private Equity is seeing a boom in demand for talent, driven by an increase in deals and an increased focus on operational improvement across ever larger portfolios. We were also surprised to see, despite the coverage that AI is already disrupting the advisory market, that there has been strong growth in hiring across consulting firms.

Finally, we look at the different dynamics of the freelance and permanent markets: Whilst the permanent market has definitely tightened, with visibly less supply, freelance is still a high supply market for talent. We hypothesise that this is more driven by the broader freelance revolution, and a sharp increase in freelancers/ interims available who have chosen to freelance for more control over their work life (which projects they do; hours worked etc.). This might also be contributing to the righter permanent market.

The Movemeon talent index

The Index is designed to give employers a read on the talent market: is it competitive? Are candidates open to new roles? Are certain industries or job types seeing more traction than others?

Below is how the index has changed over the last five years. For context, it's worth understanding the Movemeon community:

- It’s global: our 90k members are based across the world, with our main hubs in the UK, France, DACH, the Middle East, APAC and the US

- Everyone has worked in a leading consulting or accounting firm: 45% are ex-McKinsey, BCG and Bain; 30% are leading strategy firms; the remainder are the Big4

- They are future leaders and Board members: consultancies make up six of the top eight "CEO factories" (companies whose alumni become CEOs of the largest businesses). And this isn't constrained to just large businesses, with a disproportionate number of unicorns founded by consulting alumni

In terms of interpreting the numbers:

- 0-25: a very hard market to hire in. Focus on retention, as replacing people is going to be hard.

- 25-50: a hard market to hire in. Be proactive and start talent pipelining for key positions.

- 50-75: a good market to hire in. Start looking to take advantage of the market, and strengthen key positions.

- 75-100: an exceptional market to hire in. Look to bring in exceptional talent that you’ll only get a few chances to snap up.

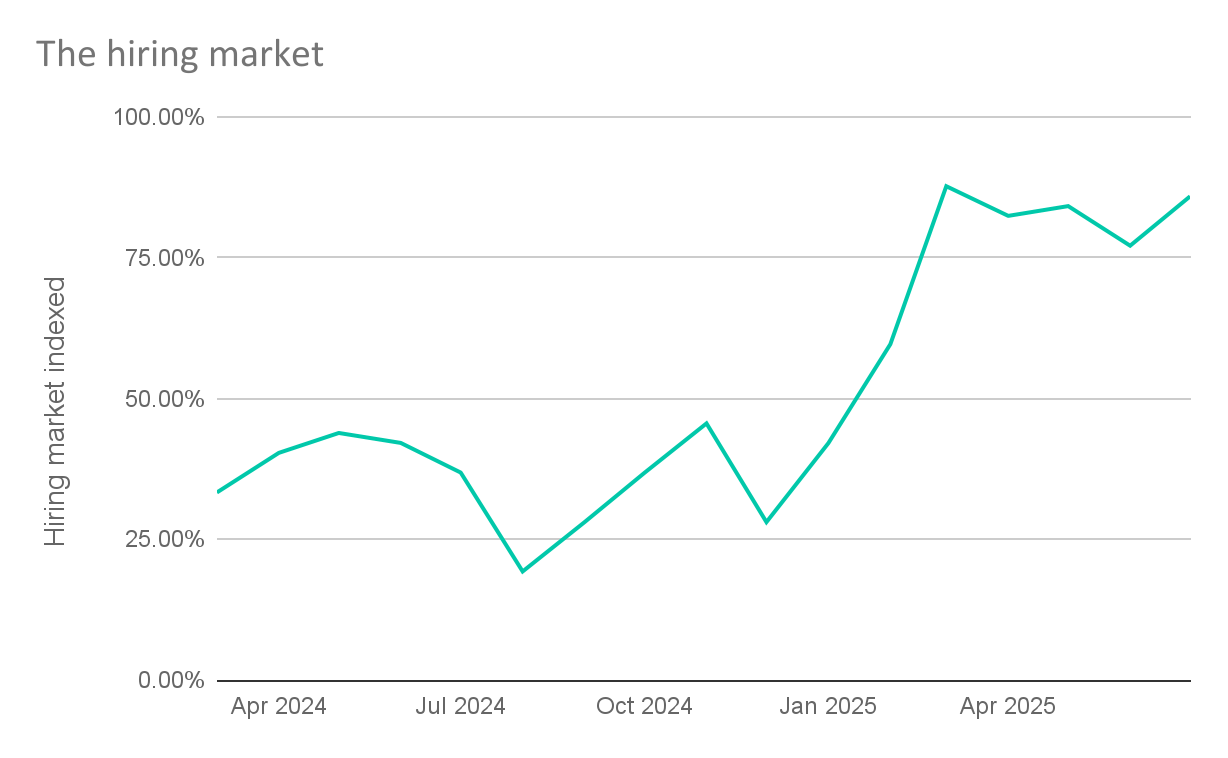

The Talent Index has dropped from 80% last quarter to 77% this quarter. This is considerably below the average over the preceding 12 months of 90, and suggests it is getting harder for companies to hire the talent they need - in other words, demand is increasing as supply decreases. For a point of comparison, it is now at the average level of 2023, where a number of companies were still struggling to hire post COVID and the Great Resignation.

To understand the drivers of this, we are looking into the changes to hiring demand across different company types.

We’ve seen a real strengthening of the hiring market

There has been a very clear strengthening in the hiring market since January 2025. We’ve seen hiring activity broadly double over the past 6 months, although this has been very varied by company type.

Whilst Private Equity, Advisory and Scale-ups are fuelling demand in the hiring market, Corporates and Large Enterprises are continue to lag. When we compare the current hiring market with the previous 12 months an even clearer picture emerges: Private Equity funds and portfolio companies have seen sustained growth, whilst hiring across Corporates and Large Enterprises has declined.

Sharp increase in hiring demand for PE-backed companies

There are two primary drivers for hiring demand for PE-backed businesses - the number of new deals and the requirement for portfolio operations support.

New deal activity: There’s been a modest increase in PE deal activity in H1 of this year. This can be shown by EY’s market pulse: there were 275 deals over $100mn vs. 200 in H1 2024. However, this is a long way short of the 400 that were averaged in 2021, and analysing the amount of dry powder in the market, it feels like these are still depressed numbers. Interestingly, based on conversations with funds over the summer period, we’ve noticed a large uptick in deals which we are confident will carry on into H2, so are expecting PE deal activity becoming an increasingly strong driver of hiring demand. This is further supported by EY’s pulse survey, with an overwhelming majority (68%) expecting an uptick in deployment.

Portfolio operations support: The requirement of portfolio operations support is driven by the size of the portfolio and the transformation requirement to achieve the VCP. We believe the increased requirement of support has been the main driver of the increased demand in H1. As funds have held onto portfolio companies for longer, there has been a multiplier effect on the support required. Not only are there more portfolio companies to support, longer holding periods require more frequent chnage to VCPs, often with more hands-on transformation/ operational support. This is against a backdrop of an increased focus on operational improvement, as interest rates have risen and financial leverage has become less effective.

An AI-driven boom for advisory firms? What’s going on

The risks posed by AI to consulting have been widely written about.

It’s clear that AI poses existential threats to the current consulting operating model. At the core of the consulting proposition is synthesising complex data, market intelligence and driving to clear recommendations. All things that AI will be able to do better than humans. It’s not an if; it’s a when.

However, we’ve seen strong growth in hiring for advisory firms. So what’s going on?

Our initial hypothesis was that boutique advisory firms pivoting to focus on AI were growing fast and therefore needing to hire. This would suggest that rather than the advisory segment growing, that it was more a case of people moving from large consulting firms to smaller ones. However, when we ran the numbers, it became clear that hiring demand was coming from both both boutique and large advisory firms.

What this suggests is that the short-term impact of AI on consulting talent has been over-played. It might also indicate another trend at play: Consultancies going through a period of growth as their clients invest in getting to grips with what AI means for them and their operating model. What remains to be seen is if this is a temporary blip, or the future of consulting.

Return of scale-up hiring - AI driven uptick, or return to normal levels?

The scale-up market has been depressed since the 2020-21 VC-driven bubble. The focus has increasingly been on the bottom line, and for many this has meant going into survival mode to elongate runways or drive towards cash-flow positive business models.

There has understandably been a big focus on AI scale-ups, and there is an increasing concern among many that there may be a new bubble forming around AI. But when we look at the hiring demand we’ve seen, it’s been broad and feels like more a return to normal levels.

When we look at the increase in hiring demand, alongside the change in the Talent Index, it’s interesting to see that despite the growth in hiring there is still a lot of supply; the Talent Index remains stubbornly at 94%, well above average in the market. This suggests that this is still a market where there is a lot of talent looking - driven by 2-3 years of depressed hiring.

In Large Enterprises, hiring levels are still low, but for those hiring, it’s hard to find the very best talent

Large Enterprise hiring is trailing well below the growth we’re seeing across Private Equity, Advisory and Scale-ups. Not only is it below the average demand it’s seen over the last 18 months, it’s also reduced in growth over the last three months.

What’s interesting is that this doesn’t mean there’s oversupply in the market. We were expecting to see a very high Talent Index - indicating there’s a lot of talent in the market looking for new roles. However, at just 58%, Large Enterprises and Corporates have the lowest value of any of our different company types. This suggests there is a real attraction challenge - the growth of PE, and to some extent scale-ups, is taking talent away from more traditional routes like joining the Strategy team of a well-recognised, large, global business.

If Private Equity and Scale-ups continue their growth - we foresee this being a hard part of the market to hire in for the foreseeable future. It’s for this reason that we’re starting to see an increase in freelance and interim demand across Large Enterprises.

Is the Freelance Revolution driving more supply in the freelance/ interim market

Whilst the Talent Index has tightened for permanent roles, it appears to be more resilient in the freelance market, where a continued over-supply of talent persists.

We’ve seen broadly consistent demand across freelance and permanent roles on the hiring side, so it feels like there is something a bit more fundamental at play on the supply side. We have written extensively on the freelance revolution that we are witnessing in the market - some of the very best talent choosing to enter the freelance market to have more control over the work they do, and their lifestyle. The more resilient talent index suggests that very strong supply on this side of the market could be the main driver. It might also help explain why we’re seeing the dip in the permanent market.

To find out more about hiring with Movemeon get in touch with our team here.

The return of the “war for talent”? It depends where…

Talent tightens, demand returns: How shifting market dynamics are creating new opportunities — and pressures — across hiring landscapes

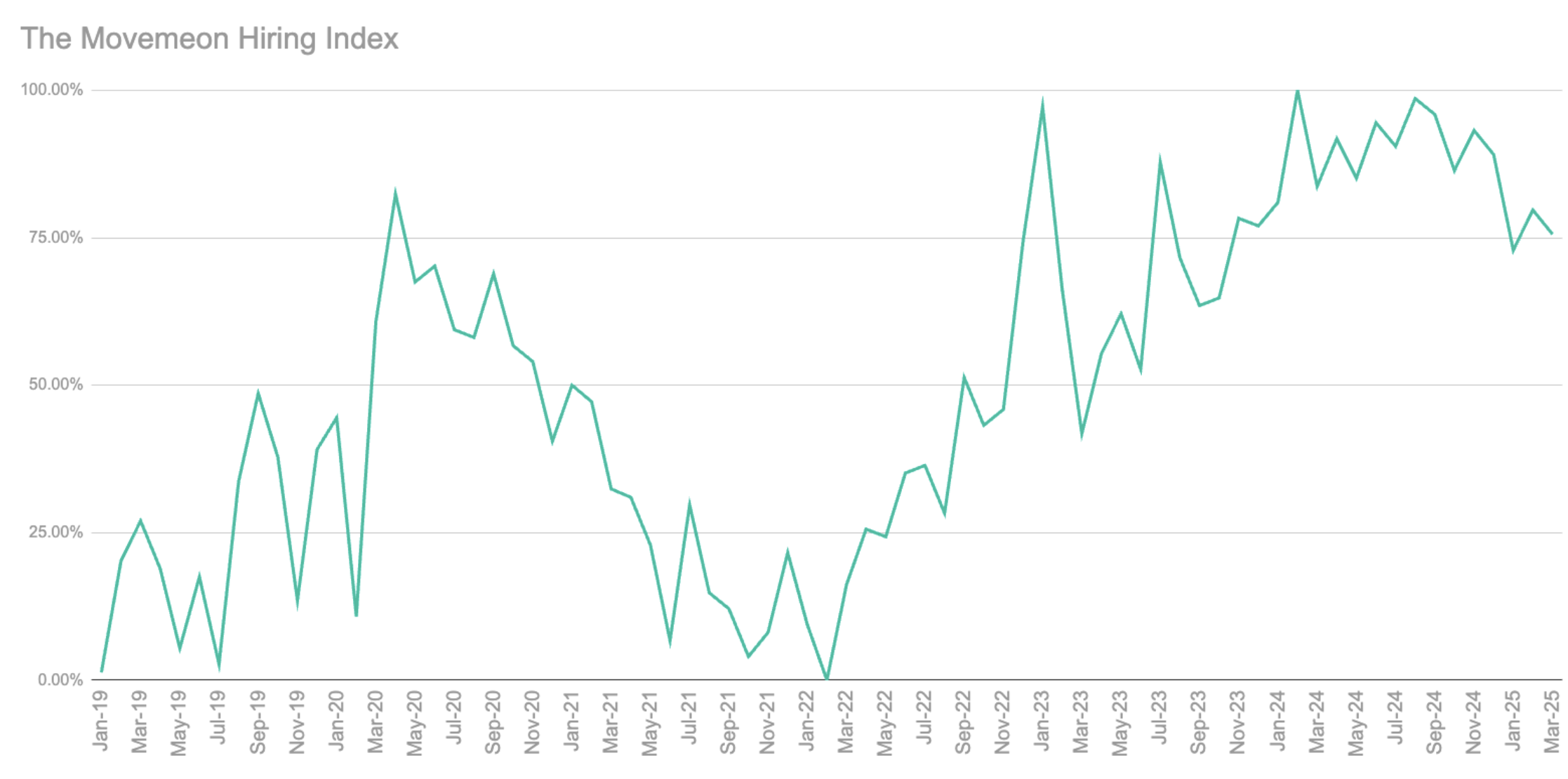

This report marks the second instalment of Movemeon’s Quarterly Hiring Analysis — a regular update designed to help hiring managers and candidates stay ahead of the market across Private Equity, VC-backed scale-ups and large Enterprise businesses. Our insights are powered by over 1.8 million data points from the Movemeon platform, giving you a clear picture of how candidate interest and hiring demand are shifting.

At the heart of this analysis is the Movemeon Hiring Index — a scale from 0 to 100 that reflects how attractive the job market is for employers. In short: a higher index means higher candidate interest per role. When the economy slows, candidate supply tends to rise, pushing the index up. When hiring demand picks up and candidate availability falls, the index drops.

To find out more about hiring with Movemeon get in touch with our team here.

This quarter, we’ve seen a strengthening in the hiring market.

After 6 months in the second half of last year with a value between 90 and 100 (the highest values we’d seen, indicating high interest in new roles), the index dropped to 75 in January and 80 in February.

We look at the drivers of this change, highlighting how a drop in the freelance market index pre-empted a drop in the permanent market index. We then look at how these trends have varied depending upon industry, finding that Private Equity is starting to lose it’s talent edge, just as there has been increased demand for hiring in the market.

We conclude that all the drivers are there for a war for talent, but that this is likely to be localised initially to Private Equity backed-companies where we’re seeing both higher hiring demand coupled with a slight decrease in candidate supply. We forecast this to further expand into consulting and potentially corporates, driven by increased demand and reduced supply respectively.

-

The Movemeon talent index

The Index is designed to give employers a read on the talent market: is it competitive? Are candidates open to new roles? Are certain industries or job types seeing more traction than others?

Below is how the index has changed over the last five years. For context, it's worth understanding who the Movemeon community are:

- It’s global: our 90k members are based across the world, with our main hubs in the UK, France, DACH, the Middle East, APAC and the US

- Everyone has worked in a leading consulting or accounting firm: 45% are ex-McKinsey, BCG and Bain; 30% are leading strategy firms; the remainder are the Big4

- They are future leaders and Board members: consultancies make up six of the top eight "CEO factories" (companies whose alumni become CEOs of the largest businesses. And this isn't constrained to just large businesses, with a disproportionate number of unicorns founded by consulting alumni

-

-

The freelance and permanent markets have broadly mirrored one another, although freelance has moved first and seen more rapid fluctuations

The freelance and interim market has broadly mirrored the permanent one, but tends to shift first — reacting more quickly to changes in business needs and macroeconomic signals. This can be seen by the permanent having a slight lag from the freelance index, as well as often slightly dampened highs and lows.

-

-

When we look at the index at a company level, we can see hiring is the hardest it has been for the past year, especially in consulting and corporates

Candidate interest in consulting and corporate roles is now at a one-year low. These sectors are beginning to feel the effects of tightening supply. In contrast, PE-backed companies — where hiring demand remains strong — are still benefiting from relatively high candidate availability, but that gap is closing thanks to slight increases in interest in start-ups/scale-ups as well as consulting.

Is the war for top talent about to heat up again?

-

The phrase “war for talent” was first coined by McKinsey in the late ’90s and resurfaced in 2022 during the Great Resignation and post-COVID hiring boom. Are we seeing a resurgence?

The answer lies in the balance between:

- Candidate supply (captured by our Hiring Index captures)

- Employer demand (based on volume and growth of roles posted)

What we’re seeing is clear: Q1 2025 was the busiest hiring quarter since early 2022. This suggests that overall demand is returning — and it’s being led by Private Equity.

In fact, PE’s share of total hiring demand has grown significantly over the past two years. As deal volume picks up and portfolio businesses push ahead with transformation plans, the ‘war for talent’ is likely to intensify, albeit localised at first.

-

Whilst we expect this war for talent to be highly localised to Private Equity initially, we are forecasting that it will expand into consulting and corporates over the course of the next year. The expansion into consulting will predominantly be demand led: increased deal flow will result in more consulting work, which will mean more hiring in a slightly dampened market. For corporates the challenge will be supply led: their historic disadvantage in hiring ex-consulting talent compared with PE or consulting has further widened, meaning a small increase in demand will have a big impact.

To find out more about hiring with Movemeon get in touch with our team here.

The most popular career paths after consulting

Consultants often leave due to "up or out" models, lifestyle, and desire to own impact; find out what career paths are the most well-trodden.

Leaving consulting for other industries is more common than staying. Many consultants move on after a few years, whether for career progression, better work-life balance, or the opportunity to take on ownership roles. If you're wondering about jobs after consulting, here’s what you need to know.

Looking for expert coaching to support your career transition? Visit OnUpBeyond for tailored career advice and coaching resources.

Why Do Consultants Leave?

From our discussions with Movemeon users and insights from our jobs board, these are the key reasons consultants transition to new roles:

- Up or out model: The traditional consulting pyramid structure pushes many professionals to leave after a few years.

- Career stepping stone: Many enter consulting with the intention of leaving once they’ve gained skills and built a network.

- Work-life balance: Long hours and frequent travel can make consulting unsustainable in the long run.

- Transferable skills: Consultants develop highly sought-after skills that are valuable across industries, from startups to private equity.

- Desire to execute: Many consultants want to move beyond advising and start executing strategies themselves.

Related Reading

- Post-Consulting Opportunities: What Pays Best?

- How to write a consulting resume - tips from an ex-consultant

Best Jobs After Consulting

Based on over 20,000 applications on Movemeon, here are the top industries for ex-consultants:

1. Corporate & Enterprise

Large companies actively recruit former consultants, often placing them in higher-level roles than their non-consulting peers. The most common functions include:

- Strategy & Transformation (Internal Strategy, Corporate Development)

- Operations & Supply Chain Management

- Growth and Business Development

- Corporate Finance

- Technology & Digital Transformation

Why consultants are a good fit:

- Experience in market research, competitor analysis, and operational improvements translates well into strategy roles.

- Consultants are skilled at navigating cross-functional teams and driving strategic initiatives.

- These roles offer a better work-life balance while still leveraging a consulting background.

Find out more about how to thrive in the corporate environment in our interviews with leaders.

2. Startups & Growth Companies

Startups offer a fast-paced, dynamic environment for consultants looking to apply problem-solving skills in a hands-on way. Ex-consultants often join startups as:

- Founders or Co-Founders

- COOs or Strategy Leads

- Chief of Staff

- Product or Growth Managers

Why consultants are a good fit:

- Consultants thrive in fast-paced, high-growth environments with shifting priorities.

- Experience in scaling operations, business development, and fundraising is highly valuable.

- Ability to identify growth opportunities and operational efficiencies makes them strong startup leaders.

- Exposure to digital transformation projects provides a foundation for tech-driven environments.

Find out what it's like to be a Chief of Staff in our interview with Penfold CoS, Aidan Curran.

3. Freelance & Boutique Consulting

For those who enjoy consulting but want more flexibility, freelancing or starting a boutique firm can be a great path. Benefits include:

- Autonomy over projects

- Higher earning potential per engagement

- Ability to specialise in a niche industry

Why consultants are a good fit:

- Broad expertise across industries makes consultants versatile for short-term strategic projects.

- Companies seek independent consultants for executive-level advisory and transformation work.

- Freelancing provides a flexible career path with strong earning potential.

4. Private Equity & Venture Capital

Many ex-consultants transition into private equity (PE) or venture capital (VC) due to their strong financial and strategic skills. Typical roles include:

- Investment Associate or Principal

- Portfolio Operations Manager

- Strategy or Due Diligence Lead

Why consultants are a good fit:

- Consultants excel at financial modeling, due diligence, and market analysis, all essential in investment decisions.

- Strong experience working with C-suite executives makes them well-suited for portfolio company strategy.

- Ability to structure ambiguous problems and make data-driven recommendations aligns with PE/VC deal-making.

Common Challenges When Leaving Consulting

1. Adapting to Corporate Hierarchies

Consultants used to flat structures may find corporate bureaucracy challenging. To navigate this, they should focus on building internal relationships, understanding decision-making processes, and adapting to longer project timelines. Seeking mentors within the organisation and leveraging their problem-solving skills to improve efficiency can also help ease the transition.

2. Adjusting to Execution-Oriented Roles

Unlike consulting, where advising is the focus, industry roles require direct ownership and execution. Former consultants can ease this transition by:

- Prioritising hands-on experience early

- Learning operational intricacies of their new industry

- Collaborating closely with teams to drive outcomes

3. Managing Work-Life Balance

Some industries, like startups and PE, can be as demanding as consulting, requiring careful career planning. Former consultants should set clear work boundaries and seek roles that align with their lifestyle goals.

FAQs

What functions within big corporates attract ex-consultants the most?

- Internal strategy, corporate development, operations, product management, and digital transformation teams commonly hire consultants.

- The choice depends on personal interests, industry trends, and networking.

What’s the biggest difference between consulting and startups?

- Consulting firms are structured and process-driven, while startups are dynamic and fast-moving.

- Consultants transitioning to startups should develop technical skills, embrace ambiguity, and be prepared for hands-on work.

How do I choose the right career path?

- What energises you? Do you prefer structured environments (corporate strategy) or high-risk, high-reward roles (startups/VC)?

- Do you want financial stability or flexibility? PE and corporate roles offer strong salaries, while freelancing provides greater independence.

- What industries excite you? Consider which sectors align with your interests and skill set.

Check out Movemeon member, Jonny's story of leaving consulting, joining a startup and going through IPO.

Find Your Next Role

Looking for your next step after consulting? Explore current opportunities on Movemeon.com.

Build Your Career with Movemeon:

- Solve a business challenge – Hire a Movemeon professional

- Advance your career – Coaching and courses for ex-consultants

- Join 40,000+ followers – Get insights on careers after consulting from our Co-Founder, Rich

What we’re doing to support your job search in 2025

Key 2024 job market trends and how Movemeon is helping candidates succeed in 2025.

2024 was a tough year to find a new role; what we’re doing to support you in 2025

2024 was a tough market to find a new job. We wanted to write this note, firstly to recognise the challenging market but also to explain what Movemeon is doing to help.

Whilst we’re proud to have grown by 15% as a business last year, we’re aware that demand for roles was at a decade-long high. Uncertainty in employers’ hiring plans has meant our values of full transparency have, at times, been hard to uphold. We implemented a number of key initiatives to make sure you were still hearing about every opportunity we were working on, and were receiving responses, and feedback, to any application you made.

This year, we are focused on offering even more to our community:

- Uncovering more opportunities for you: we shared 900 roles last year (15% more than the previous year); for 2025, we’ve built a new team to uncover more opportunities relevant to you, and have grown our US and APAC teams.

- Getting you to interview: how you are presented really matters. Last year we focused on improving screening questions to drive to the best case for an interview. This year, we’re looking to further improve how you’re presented.

- Getting feedback from every application: last year, 93.6% of applicants heard back within two weeks. Our focus this year is making that feedback as actionable and constructive as possible.

- Coaching service: we launched courses, coaching, and roundtables with a peer group of like-minded professionals to help you progress in your career in 2024. We’re going to be rapidly growing this offering in 2025.

- Executive Search proposition: as our community has got more experienced, we’ve increasingly worked on C-level roles (Chief Transformation Officer, Operating Partner, Chief Strategy Officer). To ensure you get access to more of these roles, we’re launching a Search level service for our PE and Enterprise clients in 2025.

- More insights and data: to help you make informed career decisions. This year we’ll be crunching even more of our compensation and hiring trend data, and sharing these insights with you more regularly.

How you can help one another

If there’s one thing you can do to help one another - it’s sharing relevant roles in your team/ company (“paying it forward”). 80% of our jobs last year came from our community - so thanks to all of you who have shared roles already. If you or one of your colleagues is hiring, click below and we can set up some time to see how we can help (data, insight, job description, hiring):

2024 was a tough year to move jobs

2024 was a tough market to find a new job. Our recruitment index showed as much, with demand for roles at a decade-long high. Whilst great news for companies hiring, it meant it was a very hard year for those who were looking for their next opportunity.

We’re very proud that Movemeon grew by 15%, and most importantly connected more than 2,500 of you with interviews at exciting companies. However, the tough market meant living up to our values was harder than ever before.

We built Movemeon out of our frustration with the lack of transparency in recruitment. Our values are therefore focused on empowering you in your job search: we show you all jobs for you to discover, as opposed to only calling a select few people. Uncertainties in employers’ hiring plans, longer interview processes, and increased competition, has meant our approach of full transparency has been hard: at times it would be easier not to market roles to everyone; and at times it would be easier to not give the full picture on hiring processes. However, this transparency is why we set up Movemeon, and know it’s what you value. We are therefore even more proud that our team has upheld these values during a tough market.

Uncovering more opportunities for you

We built Movemeon to help you discover great opportunities you wouldn’t have found elsewhere. We were frustrated with traditional recruitment companies, and wanted to know what jobs there were out there that would be a good fit with our experience.

Whilst we were proud to be able to share over 900 jobs with you last year, we are also aware that there are plenty more opportunities out there, and that we owe it to you to find them. We’ve therefore proactively been building our US and APAC teams - markets which are seeing rapid growth, and places we know many of you are.

We’ve been very lucky that our community (you!) shares opportunities in their team when they’re hiring. Given you understand our proposition, you know that working with us ensures you reach the best in the market. If there’s one way you can help each other, it’s paying it forward by sharing these roles. If you have any potential opportunities, please don’t hesitate to get in contact:

We have also worked hard over the last year on building a new team to identify new roles more proactively. All with the single aim of making it easier for community members to share roles with us. Early indications are positive, with 55% more jobs posted in Q4 2024 than in Q4 2023.

Getting you to interview

How you’re presented really matters.

On average, hiring managers spend just 10 seconds looking at your application. That’s why we have our success team: To give you the best chance of being interviewed.

Our success team read through your screening questions and CV in detail. And ensure that all the most relevant and important information is clearly sign-posted. They also then speak to the hiring manager, and fight your corner.

Given our business model (we only get paid if you get hired), we are incentivised to get you the job (we only get paid when clients hire) - so are always here to help present you with the best possible chance.

Getting you the feedback you deserve

Every application must receive a response. Whilst this is harder in a competitive market, there are no excuses for it not happening. As such, this is a central KPI for our team, and last year 93.6% of applicants heard back within two weeks.

And as far as possible, helpful and constructive feedback should be included. We have been working hard to ensure that we can live up to our values and provide as much information as we can about your application to you.

We are also focused this year on getting more actionable feedback from clients around why you’re not being progressed. When this is not possible, we are committed to provide you with an overview of what the candidates who are progressing have.

We know there’s a long way for us, and even further for the industry to go. This will be a continued strategic focus for us this year, and we welcome any feedback or thoughts you might have.

Launching a coaching service

Last year, Rich, our co-founder, launched OnUpBeyond to help you build your best career in or beyond consulting / finance.

We’ve always wanted to offer more to our community, and are delighted that this has come to fruition this year. Focused on how you progress in your career, it offers courses, coaching, and roundtables to connect with a peer group of like-minded professionals. If you'd like to know more:

- Register for free so you’re kept up to date with 2025’s offerings

Launching a Search proposition for our more senior members of the community

As our community has become more experienced, we’ve increasingly worked on more senior roles. In the last year we helped more companies than ever to hire Chief Executive Officers (CEOs), Chief Strategy Officers (CSOs), Chief Transformation Officers (CTOs), Chief Commercial Officers (CCOs), Chief Financial Officers (CFOs) and Operating Partners.

This level of hiring requires a more hands-on approach, for both our clients and for our candidates. As such, we are excited to be launching our Search proposition focused on Chief Strategy Officers and Chief Transformation at Enterprise businesses and Operating Partners in Private Equity (coming in Q2 2025).

If your next move will be at C-Suite level, please do keep your eyes open for the next update.

More content and insights to help you make informed decisions

This year, we are focused on driving even more insights from our rich data set. We are in a unique position to share compensation, data and insights.

In case you missed any of it, here are our most popular articles of 2024 - which cover compensation and hiring trends.

- Compensation Market Index

- Global Pay and Satisfaction Index

- Why do consultancies produce so many CEOs?

Final words

We know how hard this market is, and we are here to help however we can. We also are constantly striving to improve. So if you have any thoughts on what else we should, and could, be doing - please don’t hesitate to email us at info@movemeon.com. We thank you in advance for any thoughts (and thanks also to those of you who kindly took the time to provide feedback in 2024 - it really is enormously helpful).

In the meantime, we wanted to say a big thank you for trusting us to help, and celebrate all the new jobs you found last year…

.jpg)

Global Pay & Satisfaction Index

Benchmark your pay, working hours and job satisfaction against your peers with compensation breakdowns by industry and functional experience.

Discover Your Value with the Global Pay Index

Unlock exclusive access to the Movemeon Global Pay Index, the definitive resource for professionals seeking clarity on market compensation trends. Dive into data collected from 4,000+ global responses to benchmark your earnings across industries, seniority levels, and job types—whether permanent or freelance. With insights on pay by country, gender pay gaps, and working hours, this tool empowers you to negotiate better, plan your career, or benchmark hiring strategies.

The Global Pay Index is designed to support you:

- Benchmark Your Salary: See how your pay compares across industries, job functions, and seniority levels globally.

- Plan Your Career: Gain insights into pay trends, job satisfaction, and working hours to make informed career decisions.

- Negotiate with Confidence: Use comprehensive market data to strengthen your salary and contract negotiations.

- Explore Global Pay Trends: Understand pay variations by country and how freelance compares to permanent roles.

- Close Pay Gaps: Access gender pay gap data and identify discrepancies across industries and roles.

- Stay Competitive: Employers can use the index to attract and retain top talent with competitive offers.

Get exclusive access today and make data-driven career or hiring decisions!

To explore the full data and make informed decisions for your future - please simply provide your email address in the form below:

.png)

Why do consultancies produce so many CEOs?

The future leader factories and what it means for hiring senior leadership roles

A disproportionate number of CEOs have worked in top-consulting firms.

OnDesk recently ran the numbers - they looked at the CEOs of the US’s largest operating companies and analysed where people had started their careers. Of the top 8 most common companies, 6 are consultancies:

.png)

In this article, we look into what makes consulting alumni so well-suited to lead organisations. And what this means for you hiring for leadership positions in your team and organisation.

If you'd like to find out more about senior hiring with Movemeon get in touch with our team here.

Diverse exposure: versatility for complex challenges

Consultants are exposed to a wide array of industries, challenges, and business models during their careers. This breadth of experience enables them to adapt quickly to new environments, making them invaluable as leaders in dynamic or fast-changing markets.

High-Profile Example:

- Indra Nooyi, former CEO of PepsiCo, leveraged her experience at BCG to navigate PepsiCo’s global expansion and drive innovation in sustainability.

Consultants’ ability to analyse diverse scenarios and develop tailored solutions makes them particularly adept at addressing complex, multi-faceted challenges. This versatility can mean the difference between an executive who only fits into a niche and one who can lead across functions and industries.

Analytical proficiency: a data-driven and structured approach to leadership

Consultants are trained to analyse problems methodically, using data to guide decision-making. For CEOs, this analytical rigour is crucial in navigating uncertainty and driving strategic priorities.

High-Profile Example:

- James Gorman, Chairman and former CEO of Morgan Stanley, used his McKinsey-honed analytical skills to stabilise and grow Morgan Stanley following the 2008 financial crisis.

Hiring managers should value candidates with consulting backgrounds for their ability to synthesise complex information into actionable insights—a skill essential for steering organisations through uncertainty and change.

Strategic insight: long-term thinking for organisational growth

A key focus of consulting is strategy development—defining clear goals, aligning resources, and ensuring execution. This mirrors the core responsibilities of a CEO, making consultants natural fits for leadership roles.

High-Profile Example:

- Sheryl Sandberg, former COO of Meta (Facebook), transitioned from McKinsey to redefine Facebook’s operational strategy, contributing significantly to its growth trajectory.

Candidates with consulting experience bring a proven ability to think beyond immediate challenges and design strategies that position organisations for long-term success.

Extensive networks: access to key relationships

Consultants develop extensive professional networks through interactions with senior executives, cross-functional teams, and industry leaders. These connections often become a powerful asset in leadership roles.

High-Profile Example:

- Sundar Pichai, CEO of Alphabet (Google), utilised the network and insights gained from his time at McKinsey to transition into leadership in the competitive tech industry.

When considering candidates, hiring managers should recognise that consultants often bring with them a wealth of professional relationships that can facilitate partnerships, mentorships, and market opportunities.

Leadership development: coached for executive excellence

Consulting firms invest heavily in leadership development, equipping their employees with early management responsibility and structured training programs. Consultants are often tasked with leading client projects and managing teams early in their careers, giving them a head start in developing the skills required for executive roles.

High-Profile Example:

- Julie Sweet, CEO of Accenture, exemplifies how consulting firms prepare individuals for leadership, transitioning seamlessly into executive roles by leveraging her extensive consulting experience.

This preparation translates into candidates who are not only strategic thinkers but also adept at managing teams, driving results, and navigating high-pressure environments.

What this means for your team and your company

Consultants are a great succession plan for your Board. They will bring with them a broad skillset, proven leadership ability and clear strategic vision. Whilst this is critical in leadership roles, it’s also an invaluable skillset to have throughout your organisation.

Despite the number of well documented redundancies across consulting, it hasn’t made the market any easier to hire in. We typically find clients are looking for an ex-consultant who has already made the adjustment into “industry”, be that a PE-backed company or an Enterprise business. They’ve therefore built up a track record of delivery and “operating” over the previous 5-10 years.

If you’d like to learn more about how you would bring this type of talent to your team or company, please do let us know.

Are you overpaying new joiners?

Our hiring market analysis shows a reduced pay gap in 2024; companies may be overpaying talent.

Earlier in the year, our data showed us that it was the best time to hire in a decade, with the highest level of interest per role we’d seen since COVID. We’ve conducted further analysis, looking at what the bearing this has had on compensation dynamics in the market.

To find out more about hiring with Movemeon get in touch with our team here.

Using our proprietary data, we’ve analysed over one and a half million data points, and seen a seismic shift in the market. Two years ago, there was a large gap between the compensation candidates’ expected for a new job and how much employers were offering. Within just two years this has dropped to historic lows - suggesting that many companies “over-corrected” their salaries and are now effectively over-paying for new joiners.

In this article we look at how the compensation gap has changed over the last five years, driven primarily by supply-demand dynamics. We look at how this varies by company type, suggesting corporates have over-corrected their compensation, as well as Private Equity and Consultancies but for very different reasons.

Finally, we look at how this picture varies by alumni firm. McKinsey, BCG and Bain alumni have historically commanded a premium in the market, but we’re seeing early indications that this premium is decreasing. MBB expectations have only increased by a modest (and below inflation) level of 2% compared with 4% for the Big4 and 6% for boutiques.

Introducing the Movemeon compensation index and what it says about the market

Below you’ll see how the Movemeon compensation index has tracked over the last five years. We’ve analysed over one and a half million data points going back five years, looking at the gap between expectation and reality when it comes to comp. We see this as a measure of “friction” in the market, and an early indicator of inflationary pressures on wage growth.

For the numbers to make sense, it’s worth a quick recap of who’s in the Movemeon network;

- It’s global: our 75k members are based across the world, with our main hubs in UK, France, DACH, Middle East, APAC and US

- Everyone has worked in a leading consulting or accounting firm: 45% are ex-McKinsey, BCG and Bain; 30% are leading strategy firms; the remainder are the Big4

- They are future leaders and Board members: it’s well documented that McKinsey is the largest future leader factory in the world. The number of ex-consulting and accounting professionals leading companies (from Fortune 500 to PE and VC backed scale-ups) is astounding

How to interpret the numbers:

- 0-25: There’s only a small difference between candidate expectations and compensation offered In other words, it’s a highly efficient market

- 25-50: There’s a manageable difference between candidate expectations and compensation offered.

- 50-75: There’s a marked gap between candidate expectations and compensation offered - a high friction market.

- 75-100: There’s a large and unsustainable gap between candidate expectations and compensation offered - a very high friction market

Supply-demand in the hiring market is the driver behind the compensation dynamics

When we plot our hiring and compensation indexes together, it’s clear there’s a very strong causal relationship (an 85% negative correlation). The more in demand ex-consultants are, the more their compensation expectations increase, resulting in a larger compensation gap between job offers and expectations.

Are you now over-paying for new joiners? The compensation gap is at an all-time low

Over the past 5 years, we’ve seen the gap between expectations and job offers hit historic highs of 22% in 2021, before falling way down to 6%, -9% below the historic average.

We had assumed the drivers of the decrease in this gap were candidates re-adjusting their expectations downwards. This is historically what we’ve seen in very competitive hiring markets.

But this has not been the case. Over the past year, compensation expectations within our community have still increased at a healthy rate. The real driver of the expectation gap has been a very high increase in compensation being offered for jobs. This is clearly unsustainable in the longer-term, and feels like an over-correction in response to the higher consulting salaries and candidate expectations we saw in 2022-23.

For our latest salary information, you can view our benchmarking here.

Over-correction, hard to recruit talent, or paying for the best - how PEs, scale-ups, consultancies and advisories have reacted

When we look at our compensation index by company type, there are some very interesting trends.

Large corporates have a compensation gap of just 2%. This is much lower than historic averages, suggesting they have overcorrected compared with candidates’ expectations.

Scale-ups on the other hand have a gap of 13%. This is in line with historic averages and suggests that a focus on profitability combined with lower levels of VC-funding have ensured there hasn’t been an over-correction.

In the advisory space the picture is quite surprising. It’s been widely reported that it’s a tough market for consultancies, however, what our data shows is that those who are recruiting are prepared to pay a large premium - 8% in large consultancies, 5% in boutiques. We think this is being driven for two reasons: firstly, firms that are recruiting are growing, and as such are in a position to be paying for high performing (more expensive) talent; secondly, it is a hard market in which to attract ex-consultants given slow growth in the industry as a whole. To make it more appealing, bigger packages are being offered.

Finally, Private Equity is also paying a premium to outstrip expectations. This comes as no surprise and is also in line with historic norms in the sector. Private Equity is focused on attracting the very best, and as such is prepared to pay top decile compensations.

Compensation trends offer further evidence that McKinsey, BCG and Bain have been harder hit by the downturn than other strategy firms

When you look at how compensation expectations have changed by alumni firm, an interesting trend emerges. McKinsey, BCG, Bain alumni have seen the lowest increase in their expectations - a modest (and below inflation) figure of 2.3%. This is broadly in line with other strategy firms, but under half what we’re seeing alumni of boutiques and the Big4 demand.

Despite the higher increase in expectation from boutique and Big4 alumni, McKinsey, BCG and Bain alumni are still paid a premium of over 12% compared to the median compensation.

If you’d like to find out more about how Movemeon can support your hiring, please get in touch.